Media release on third quarter 2011

- Better results in third quarter and organic growth in four of the five Group regions

- Higher sales volumes in cement, aggregates and ready-mix concrete over nine months and in the third quarter

- Latin America and Asia/Pacific on growth path

- Europe and North America lack key stimuli

- As of end of September, operating EBITDA impacted by CHF 458 million, due to the strong Swiss franc

- Declining operating EBITDA as per end of September due to cost increases which could not yet be passed on completely to sales prices

- For the current financial year, Holcim expects a like-for-like operating EBITDA that will be close to last year’s level

Download PDF-version of this media release

Table: Third quarter results 2011 - Group

As expected, many emerging markets enjoyed brisk construction activity. However, in the eurozone and in North America, growth mainly remained restrained.

Despite this, Holcim increased its third quarter and nine months sales volumes for cement, aggregates and ready-mix concrete. Only asphalt declined slightly.

The higher demand was accompanied by above-average inflation for energy, transport and raw materials. These cost increases could for the time being only partially be passed on to sales prices. However, the Group's operating EBITDA was also negatively impacted in the amount of CHF 458 million by the strong Swiss franc, and by the fact that, contrary to last year, sales of CO2 emissions certificates in Europe are still outstanding. Costs which could be influenced were kept well under control.

On a like-for-like basis, operating EBITDA was higher than last year in Latin America and Asia Pacific. Europe fared less well, mainly because of the still outstanding sales of CO2 certificates. In the US, the ongoing insufficient demand for construction materials and the stabilization of prices at a low level both impacted results.

(Details on Group regions after the outlook)

Development of sales volumes

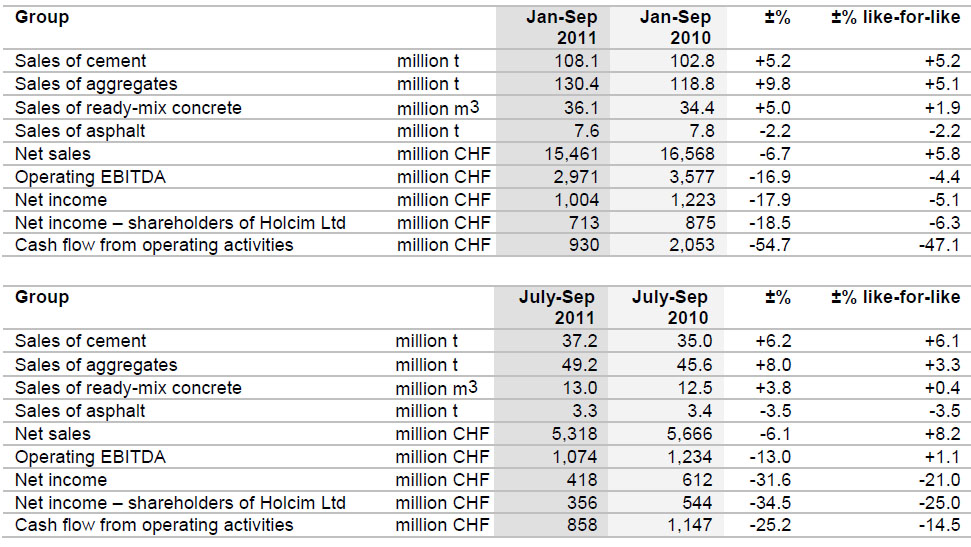

Consolidated cement deliveries increased by 5.2 percent to 108.1 million tonnes by end of September 2011. Shipments of aggregates increased by 9.8 percent to 130.4 million tonnes, and ready-mix concrete rose by 5 percent to 36.1 million cubic meters.

The cement segment in Group region Latin America achieved the strongest rise, followed by Asia Pacific and Europe. Latin America also ranked first in terms of aggregates, while Asia Pacific too achieved double-digit growth. North America experienced a particularly sharp rise in sales of ready-mix concrete.

Financial results

Consolidated net sales decreased by 6.7 percent to CHF 15.5 billion, mainly because of exchange rate factors. On a like-for-like basis, it rose by 5.8 percent. Operating EBITDA fell by 16.9 percent to CHF 3 billion, but on a like-for-like basis the decline came to a smaller 4.4 percent, and organic growth reached 1.1 percent in the third quarter. In particular, the Group companies in Russia, Singapore, Indonesia, Colombia as well as Holcim Australia made larger contributions in Swiss francs to the result. While many other Group companies improved their results in local currency terms, in the consolidated financial statements these successes were cancelled out by the strong Swiss franc however. The Group company in the Philippines was among those to see their performance hit by rising costs and regional falls in selling prices. The operating EBITDA margin reached 19.2 percent (nine months 2010: 21.6) despite the still outstanding sales of CO2 emissions certificates. Signs of a slight improvement in operating EBITDA did start to emerge in the third quarter, as demand clearly increased, particularly in the emerging markets and in North America. As a result of the increase in net current assets, one-off tax refunds in the previous year and lower operating EBITDA, cash flow from operating activities came to CHF 930 million.

From January to September 2011, net income decreased by 17.9 percent to CHF 1 billion and net income attributable to shareholders of Holcim Ltd declined by 18.5 percent to CHF 713 million.

In the past twelve months, net financial debt decreased by 4.7 percent from CHF 12.7 billion to CHF 12.1 billion, due to cash flow from operating activities and the depreciation of various currencies against the Swiss franc.

Outlook

As a leading producer of construction materials, Holcim heavily depends on developments in economic activity. In Europe, the demand for construction materials should remain solid in many places. In North America the Group expects a slight improvement in the construction sector. Most emerging markets in Latin America and Asia should remain on track for growth. No change is anticipated in business conditions in Group region Africa Middle East. The sharp global rise in energy, raw material and transportation costs call for further price adjustments. This and continuous, consistent cost management are focal points at all levels of the Group. For the current financial year, Holcim expects a like-for-like operating EBITDA that will be close to last year’s level.

The Group will be successful in securing its share of future growth in the emerging countries due to its consistently expanded presence in these markets. In Europe and North America, Holcim's lean cost structure will enable it to benefit more than average from economic recovery.

Detailed information on Group regions:

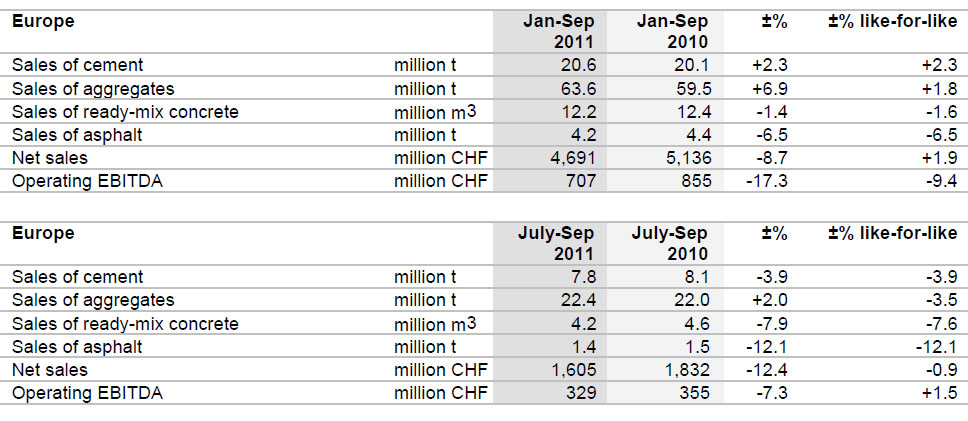

Positive volume development in Europe in cement and aggregates

In Group region Europe, demand increased. However, there was still a lack of building material intensive projects. More construction work is ongoing in Russia, primarily in the greater Moscow area. In Group region Europe, Holcim sold more cement and aggregates in the first nine months of 2011, despite the difficult market situation in Spain. Ready-mix concrete deliveries nearly matched the previous year’s level.

Table: Third quarter results 2011 - Europe

Aggregate Industries UK saw its shipments of aggregates fall back slightly amid declining exports to continental Europe; asphalt volumes also decreased. Ready-mix concrete volumes were supported by supplies for major construction projects in London.

Holcim France achieved higher delivery volumes in all segments, with the aggregates and ready-mix concrete acquisitions made in Alsace at the beginning of the year having a positive effect. The price pressure eased slightly in the course of the year. In Belgium, competition remained fierce, putting pressure on cement and ready-mix concrete prices.

Holcim Germany benefited from infrastructure projects and increased its sales volumes in all segments. Primarily in the ready-mix business sales prices remained under pressure. The Group company in southern Germany also recorded higher sales across its entire product range, due in part to an increase in exports to Switzerland. In Switzerland, where conditions for the construction sector were robust, Holcim achieved an increase in volumes in all segments despite growing pressure on prices.

Due to slow construction activity and deconsolidations, sales volumes at Holcim Italy decreased. However, cement prices started to recover slightly from the low level of 2010. Construction projects in preparation for the 2015 World Expo in Milan generated some positive stimuli. At Holcim Spain, demand was depressed by the lack of activity in the private house-building sector and the decline in public spending on construction projects. Holcim Spain decided to close 25 ready-mix concrete plants; this led to non-recurring costs.

In Eastern and Southeastern Europe the construction sector mainly stagnated. A few infrastructure projects made a positive impact on demand, so most Group companies increased their shipments of cement. The strongest volume increase was achieved in Romania and Slovakia. The aggregates segment also recorded an increase in sales volumes, driven by the Group companies in the Czech Republic, Romania, Croatia and Bulgaria. Overall, volumes of ready-mix concrete declined slightly despite positive trends in Croatia, Romania and Serbia. Due to the difficult market conditions, Holcim Hungary lagged behind its previous-year figures in all segments.

In Russia, Holcim benefited from a revival in construction activity in the Greater Moscow area and increased its sales of cement significantly. Due to the brisk demand, prices also increased. At Garadagh Cement in Azerbaijan cement deliveries declined in the face of a sharp rise in imports.

Cement sales in Group region Europe increased by 2.3 percent to 20.6 million tonnes in the first nine months of 2011. Deliveries of aggregates rose by 6.9 percent to 63.6 million tonnes. However, volumes of ready-mix concrete decreased by 1.4 percent to 12.2 million cubic meters.

Operating EBITDA for Group region Europe decreased by 17.3 percent to CHF 707 million. In Swiss franc terms, the results were depressed by a combination of the weak euro and the still outstanding sales of CO2 emissions certificates. These came to CHF 11 million, compared to CHF 75 million during the same period last year. Many Group companies were only partially able to offset the rise in costs with price increases. Better results were achieved primarily at Holcim Russia and Holcim Switzerland. Internal operating EBITDA development came to -9.4 percent, and was positive with 1.5 percent in the third quarter.

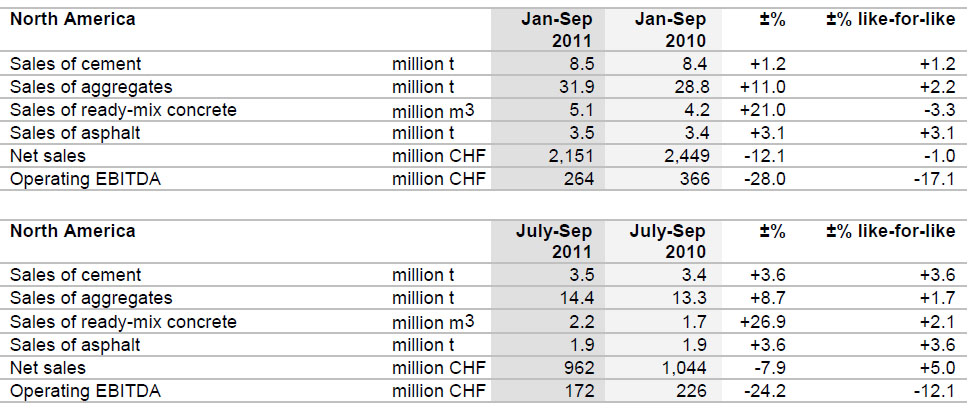

Slightly better demand for building materials in North America

There is still a lack of important stimuli in the US construction sector. However, public road-building did create some activity, primarily in the third quarter. Canada's economy developed weakly in those markets relevant to Holcim.

Table: Third quarter results 2011 - North America

In August, cement sales by Holcim US exceeded one million tonnes for the first time since October 2008. Demand remained weak in the southern US states.

Aggregate Industries US significantly increased its deliveries of aggregates, ready-mix concrete and asphalt. In the aggregates segment, the Group company benefited from slightly stronger demand in the mid-Atlantic region and in Minneapolis/St. Paul. Sales of asphalt increased in the northeast of the country and in the west central region. The full takeover in March of Lattimore Materials strengthened the market presence in Texas.

Holcim Canada felt the decline in construction activity in all relevant markets. In Ontario, construction activity increased again slightly in the house-building segment, but commercial construction remained sluggish. On balance, the Group company sold less cement and ready-mix concrete. Volumes increased in the aggregates segment, but there was less demand for high-grade gravel and prices came under pressure. However, like-for-like, operating EBITDA of Holcim Canada improved by 3.8 percent in the third quarter.

Consolidated cement shipments in Group region North America increased by 1.2 percent to 8.5 million tonnes. Primarily due to an acquisition, deliveries of aggregates increased by 11 percent to 31.9 million tonnes, and ready-mix concrete sales were up by 21 percent to 5.1 million cubic meters.

Operating EBITDA for Group region North America fell by 28 percent to CHF 264 million. All three Group companies were unable to improve on their previous year’s results. Higher energy and distribution costs had a negative impact on the operating result of Holcim US. Expenses were also incurred for the temporary closure of the Catskill plant in New York State. Due to increased production costs Aggregate Industries US recorded lower results. At Holcim Canada, rising price pressure, particularly in the ready-mix concrete business, and higher cement manufacturing costs had a negative impact on the income statement. Internal operating EBITDA development in Group region North America came to -17.1 percent (third quarter 2011: -12.1).

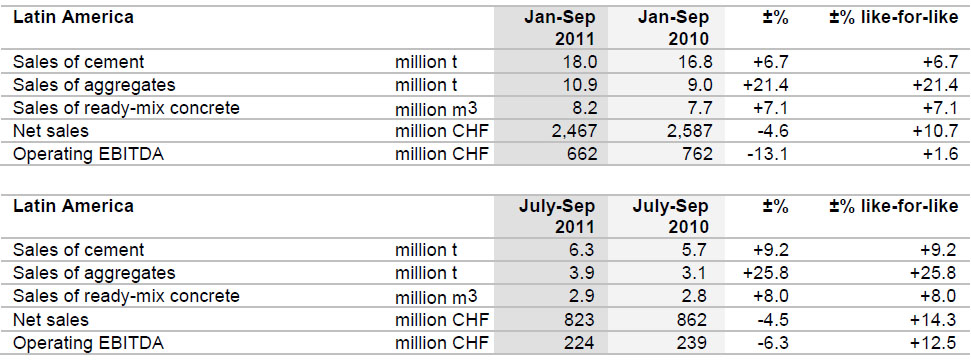

Solid markets in Latin America

In Group region Latin America, the economy made positive headway in most countries. Numerous infrastructure projects supported demand for building materials, particularly in Brazil, Argentina, Colombia and Chile. All Group companies sold more cement than in the previous year and nearly all also increased their sales of aggregates and ready-mix concrete.

Table: Third quarter results 2011 - Latin America

The Mexican construction sector recovered a little due to the national infrastructure plan and private house-building activity. However, commercial construction projects remained thin on the ground, and some public sector construction projects continued to be postponed. However, Holcim Apasco sold more building materials in all segments, with aggregates exhibiting strong growth.

El Salvador enjoyed good levels of construction activity. The local Group company increased sales across all segments, in some cases significantly so. Holcim Costa Rica and Holcim Nicaragua combined increased shipments of aggregates and ready-mix concrete.

The Colombian economy continued to develop well. There were particularly sharp increases in demand for building materials in the infrastructure segment, as well as in the residential and industrial construction sectors. The expansion of grinding capacity at the Nobsa plant allowed the Group company to sell significantly more cement, and sales of aggregates and ready-mix concrete also made good progress. Thanks to road-building and infrastructure projects, Holcim Ecuador increased deliveries of construction materials in all segments. Indeed, demand was such that clinker had to be bought in occasionally.

In Brazil, the construction sector remained on its upward trend. Due to the high capacity utilization rate, Holcim Brazil concentrated on sales of higher value cement types. Nevertheless, shipments also slightly increased. With the commissioning of the second kiln line at the Barroso plant, from 2014, Holcim Brazil will increase its cement capacity in this dynamic growth market by 2.6 million tonnes to a total of 7.9 million tonnes. Deliveries of aggregates and ready-mix concrete remained stable.

Argentina's construction sector benefited from public sector investment ahead of the country's presidential elections, but private investors tended to hold back. Minetti, which started marketing under the name Holcim Argentina in September, increased sales of cement and aggregates. Shipments of ready-mix concrete declined following the completion of infrastructure projects. In a difficult competitive environment, Cemento Polpaico in Chile experienced good volume growth in all segments.

Consolidated cement sales in Group region Latin America increased by 6.7 percent to 18 million tonnes. Deliveries of aggregates rose by 21.4 percent to 10.9 million tonnes. Deliveries of ready-mix concrete also advanced by 7.1 percent to 8.2 million cubic meters.

As a result of rising energy costs, particularly for petcoke, higher distribution costs and the fact that prices could not yet be adjusted everywhere, operating EBITDA declined despite the volume growth by 13.1 percent to CHF 662 million. In Ecuador, higher maintenance costs and clinker purchases affected the income statement. The strong Swiss franc impacted above all on the results of the Group companies in Mexico, Ecuador and Argentina. Worthy of particular mention is the gratifying result achieved by Holcim Colombia. In Group region Latin America, internal operating EBITDA growth came to 1.6 percent and reached 12.5 percent in the third quarter.

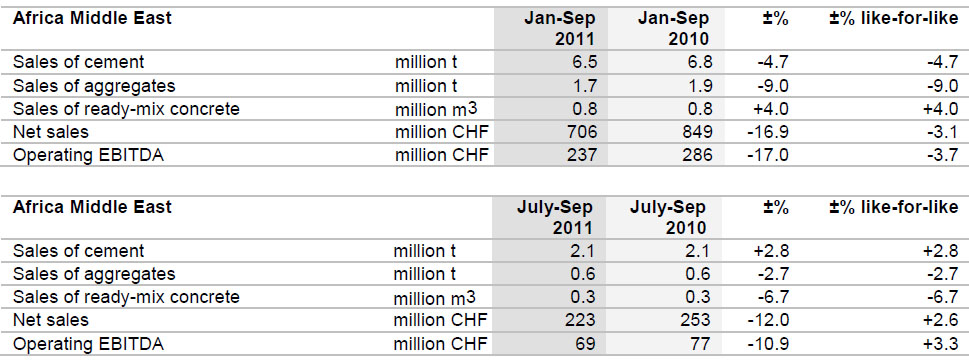

Unchanged market conditions in Africa Middle East

In Morocco and Lebanon, the two most important markets in this Group region, construction activity remained brisk. Whereas in Morocco demand was supported by government stimulus programs in the social housing and infrastructure sectors, in Lebanon sales of construction materials were supported by private house-building.

Table: Third quarter results 2011 - Africa, Middle East

In an increasingly tight competitive environment, Holcim Morocco sold less cement and aggregates. However, a clear increase was achieved in sales of ready-mix concrete, mainly in the region of Fès. Despite some project delays at construction sites in Beirut, Holcim Lebanon sold slightly more cement and ready-mix concrete; exports remained negligible.

The Indian Ocean companies sold more cement and ready-mix concrete. The Group companies in Mauritius and La Réunion in particular witnessed positive volume development, as did the Group company in Madagascar. Deliveries of aggregates declined slightly. In West Africa and the Arabian Gulf, volumes sold by the operations managed by Holcim Trading remained quite stable. Ivory Coast markets in particular firmed again slightly.

Cement sales in Group region Africa Middle East decreased by 4.7 percent to 6.5 million tonnes, mainly due to the volume decline in Morocco. Aggregates also contracted by 9 percent to 1.7 million tonnes, while ready-mix concrete sales rose by 4 percent to 0.8 million cubic meters.

Compared with the previous-year period, the operating EBITDA of Group region Africa Middle East declined primarily due to the currency impact by 17 percent to CHF 237 million. The internal operating EBITDA development came to -3.7 percent, but was positive in the third quarter with 3.3 percent.

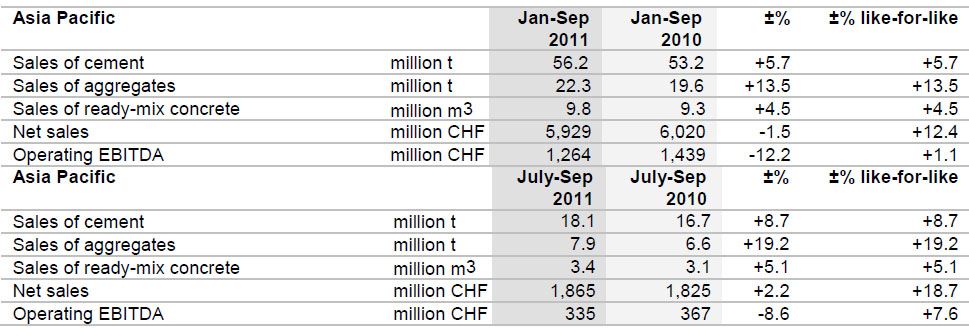

Continuing volume growth in Asia Pacific

The Asian markets remained on their path of growth driven by brisk demand for building materials. Public spending on infrastructure was important in a number of countries, with cement consumption also increased by private residential and commercial construction activity. In Oceania, construction activity failed to gain real momentum due to a lack of concrete-intensive projects.

Table: Third quarter results 2011 - Asia Pacific

In India, demand in the private construction sector declined slightly, particularly in the south of the country, due to higher interest rates and inflation. By contrast, the government's extensive road-building program boosted the construction sector in virtually all parts of the country. Due to the successful commissioning of additional capacity, ACC achieved a significant increase in cement volumes. Sales of ready-mix concrete remained at previous year’s level. Ambuja Cements increased cement deliveries further in the northern parts of the country. In September, the Group company took a 60 percent majority stake in Dirk India, a fly ash dealer, thereby strengthening its activities in the production of composite cements.

In Sri Lanka, the construction boom continued in a favorable market environment. Holcim Lanka had to import cement to meet the strong demand, but pressure on prices increased significantly. Holcim Bangladesh also delivered more cement.

Siam City Cement in Thailand saw a rise in sales of cement in the growing domestic market. Deliveries of aggregates and ready-mix concrete rose substantially. Holcim Malaysia also sold more cement and ready-mix concrete amid positive market conditions. In Singapore shipments of ready-mix concrete declined slightly.

In Indonesia, the construction sector remained on track for growth due to government infrastructure projects and expansion work in the industrial sector. Major projects in the transport and energy sectors, coupled with the construction of office buildings, shopping centers and entire residential developments fuelled a dynamic market. Across its whole product range Holcim Indonesia sold significantly more building materials than during the same period last year.

The Philippine construction sector felt the lack of public sector investment activity. The situation improved slightly from August onward as both the government and private investors increasingly returned to the market to develop projects. During the first nine months of the year, cement deliveries nevertheless declined in a competitive market. However, sales of aggregates and ready-mix concrete increased.

Construction activity in Oceania remained subdued. Despite a boom in Australia's mining industry, there was a clear lack of cement and concrete intensive projects. Road-building in the aftermath of the floods impacted positively on cement demand only from the third quarter. On balance, Cement Australia sold less cement. Holcim Australia delivered more aggregates on both the east and west coasts, and increased deliveries overall in this segment. In the third quarter, shipments of ready-mix concrete also picked up slightly. Sales were more moderate in the pipe and concrete products segment at Humes due to project delays. Holcim New Zealand sold less building materials in all segments. This reflects private investors' uncertainty over the future development of the economy.

Consolidated cement shipments in Group region Asia Pacific climbed by 5.7 percent to 56.2 million tonnes. Aggregates saw an increase of 13.5 percent to 22.3 million tonnes. Deliveries of ready-mix concrete rose by 4.5 percent to 9.8 million cubic meters.

Operating EBITDA in Group region Asia Pacific decreased by 12.2 percent to CHF 1.3 billion. Stronger results were achieved above all by the Group companies in Thailand, Vietnam, Malaysia, Singapore and Indonesia. However, negative currency effects depressed the results of all Group companies. Furthermore, at Cement Australia one-off costs for the closure of the Kandos plant occurred. Like-for-like, ACC exceeded its previous year result, but it proved impossible to pass on the full impact of inflation to prices. The internal operating EBITDA growth came to 1.1 percent and even reached 7.6 percent in the third quarter.

* * * * * * *

Holcim is one of the world's leading suppliers of cement and aggregates (crushed stone, gravel and sand) as well as further activities such as ready-mix concrete and asphalt including services. The Group holds majority and minority interests in around 70 countries on all continents.

* * * * * * *

This media release is also available in German at www.holcim.com/news.

* * * * * * *

Corporate Communications: Tel. 41 58 858 87 10

Investor Relations: Tel. 41 58 858 87 87

* * * * * * *

Additional information such as the Third Quarter Interim Report 2011 is available at www.holcim.com/results.

Press conference: November 9, 2011, 09:30 a.m. Hagenholzstrasse 85, Zurich

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}